Hyeyoung Park (MBA, 2023)

Ⅰ. What if we could detect a real estate bubble?

In 2021, the real estate market entered a recession as the bubble burst. The government is hastily preparing policy to activate the market, but it doesn’t seem to be working as planned. However, if we could detect the real estate bubble in advance, wouldn’t it be possible to prevent the market from entering a recession?

The impact of the real estate bubble

The impact of the real estate bubble was immense. Apartment prices recorded the largest decline and Seoul’s overall housing sale prices experienced the biggest drop since the subprime mortgage crisis.

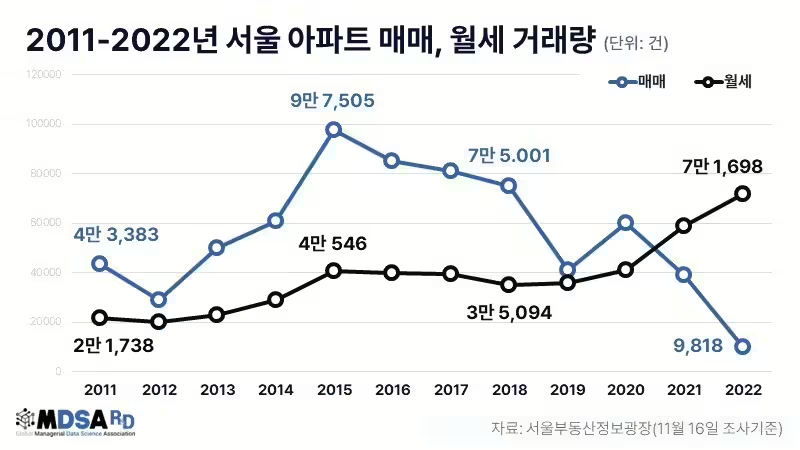

Along with the decline in real estate prices, real estate transactions have also decreased as financial authorities sharply raised the base rate to reduce liquidity. In Seoul, homeowners are even offering to cover maintenance fees, moving costs, and luxury bags to promote leases and sales, but unlike before, transactions are not happening as actively. As seen in Figure 1, the number of apartment transactions in Seoul from January to September 2022 fell below 10,000, a decrease of 73.7% compared to the last year.

Many experts are concerned that the real estate recession could directly lead to a shock in the economy. To prevent this, they argue that the current real estate policies must be swiftly overhauled with new taxation policies suited to the era of high interest rates. They think the comprehensive real estate tax and capital gains tax are too burdensome, and coupled with high loan interest rates, real estate transactions are not occurring actively. Therefore, they suggest that easing real estate taxes and removing regulations are necessary to boost transaction volumes.

On the other hand, hastily changing real estate policies could be risky. The massive liquidity and low-interest rate environment caused by the global pandemic led to speculative behavior among people in their 20s and 30s, trapping many young adults in debt. Considering this reality, indiscriminately easing or removing real estate regulations could be dangerous. Therefore, the government should maintain appropriate levels of regulation to curb speculation and ensure that housing opportunities are available for real homebuyers.

Governments have alternated between these two approaches to find policies that would minimize the impact of housing bubbles. However, they have been unable to find an ideal solution that satisfies everyone. Excessive regulation risks violating the basic market principle that prices are determined by supply and demand, while too much leniency can lead to market disruptions like speculation, over-leveraging. It’s extremely difficult to strike a balance in policy-making that satisfies everyone’s needs.

What if we could identify a real estate bubble in advance?

Many people fail to recognize a bubble in the real estate market until prices crash. This is because accurately measuring the intrinsic value of real estate is difficult. As a result, most market participants mistake rising property prices for an increase in intrinsic value and get swept up by the decisions of others, leading to a bubble. When the bubble bursts, the inflated asset prices drop, which can lead to increased household debt, large-scale bad debts for financial institutions, and, in severe cases, an economic recession.

However, what if we could detect a real estate bubble in advance? It could help resolve many of the concerns mentioned above. The government would be able to identify overheating in the real estate market early and take an action before the bubble negatively impacts the real economy. Moreover, given the high level of global interconnectedness today, a bubble in one country can have significant effects on the global economy, making the prediction of bubbles increasingly important.

In this article, I will explain the steps taken to identify factors related to a real estate bubble and statistically verify them. Specifically, we will examine whether the “winner’s curse”, often cited as a cause of real estate overheating, truly corresponds to a bubble by using regression analysis and statistical testing.

II. The History of Bubbles and the Reasons They Recur

A bubble refers to a phenomenon where the price of a specific asset significantly exceeds its intrinsic value due to excessive demand. This typically occurs when the economy becomes overheated.

When a bubble bursts, it leads to massive losses for investors and delivers a significant blow to financial institutions whose main business is providing mortgage loans. This could result in systemic risk across the financial market.

The History of Bubbles

Bubbles have historically repeated themselves multiple times in the global financial market. Examples include the Dutch Tulip Bubble of the 1630s, the South Sea Bubble in Britain during the 1720s, the Japanese real estate and stock market bubble of the 1980s, the Dot-com Bubble of the 1990s, and the U.S. housing bubble of the 2000s.

Let’s first take a closer look at the Japanese real estate bubble. In the early 1980s, as the yen surged and Japan’s trade situation worsened, the Japanese government implemented monetary policies to stimulate the economy. With increased liquidity in the market, speculation was fueled, leading to a bubble between 1985 and 1989, during which the value of Japanese stocks and urban land tripled. At the peak of the real estate bubble in 1989, the value of the Imperial Palace grounds in Tokyo exceeded the total real estate value of the state of California. Ultimately, the bubble burst in 1991, leading to Japan’s prolonged economic stagnation, known as the “Lost Decade.”

Next, let’s look at the U.S. subprime mortgage crisis. After the dot-com bubble burst, many investors, learning from the experience, shifted money into real estate, which was considered a relatively safe asset. As a result, U.S. housing prices nearly doubled between 1996 and 2006. Additionally, as interest rates dropped, people rushed to buy homes using mortgage loans. However, to control the skyrocketing housing prices, the U.S. government sharply raised interest rates, leading to a wave of defaults by subprime borrowers who were unable to repay their loans. This turned mortgage-backed securities into worthless assets and pushed banks and other financial institutions on the brink of collapse.

The U.S. subprime mortgage crisis had a significant impact on South Korea as well. Major hedge funds and investment banks, including prominent U.S. financial institutions like Bear Stearns and Lehman Brothers, faced bankruptcy. Learning from this, foreign investors began favoring safer assets, causing significant volatility in the Korean foreign exchange market. As the interest rate spread between the U.S. and South Korea widened, the carry trade became widespread. It leads to negative effects on both the domestic financial market and the real economy in Korea.

The Reasons Bubbles Recur

The main method of detecting a real estate bubble is by examining the ratio between the money supply and the market capitalization of apartments. Generally, when the money supply increases, the value of money declines, leading to a rise in apartment prices. However, if the gap between the growth rates of the money supply and apartment market capitalization becomes unusually large, it may indicate a bubble. This suggests that apartment prices are rising independently of the available money supply. In November 2021, when the bubble was at its peak, the ratio of apartment market capitalization to the money supply soared to 147%. This shows that apartments were highly overvalued compared to their intrinsic value.

So why do bubbles continue to recur in cycles? Despite experts consistently presenting objective indicators, such as the one mentioned above, and warning about signs of a real estate bubble, why do people persist in risky behaviors like over-leveraging (“all-in” borrowing) and speculative investments (“betting with borrowed money”)?

Robert Shiller, the 2013 Nobel Prize winner in economics, argued in his renowned book “Irrational Exuberance” that most market participants do not fully understand the true nature of the market. He further stated that people often don’t even care about why the market might be undervalued or overvalued. In such an environment, people’s investment decisions are heavily influenced by easily accessible information. In other words, instead of conducting deep quantitative and qualitative analysis, most investors are drawn to shallow, hearsay-like information, leading them to make decisions that are closer to gambling.

The core principle of a bubble can be summarized in one word: “Herd effect”. In these situations, the independence of individuals breaks down, leading to irrational decisions made collectively.

III. Characteristics of the Real Estate Auction Market in Korea

In this section, let’s explore why we should examine the auction market as a tool for predicting bubbles in the real estate sales market.

Recently, the real estate sales market has suffered a transaction freeze. The auction market typically comes into the spotlight when the real estate market enters a downturn. Due to the bleak outlook, competition for successful bids significantly decreases, and the bid price ratio — the ratio of the final bid to the appraised value — also drops noticeably. This, in turn, increases the incentive for investors.

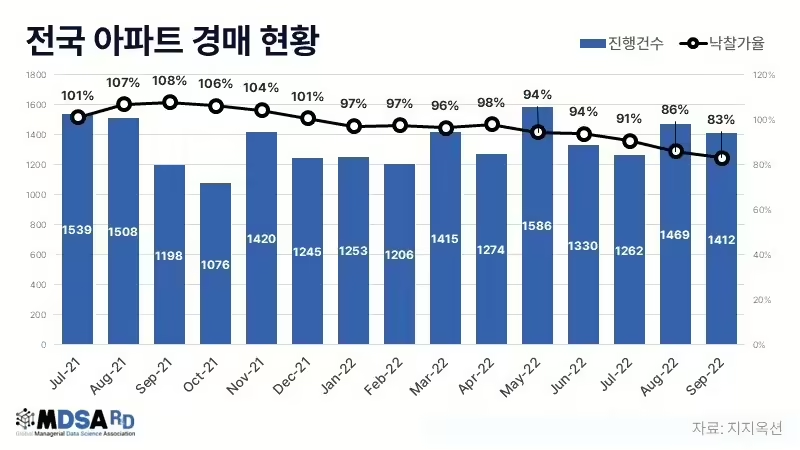

In fact, the auction market appears to be reviving. According to a report published by the court auction specialist firm, Gigi Auction, the number of apartment auctions nationwide in October 2022 was 1,472, marking an upward trend after recording 1,330 cases in June of the same year. Additionally, the nationwide apartment bid price ratio in October 2022 was 83.6%, only a 0.5 percentage point increase from 83.1% in September of the same year, which was the lowest level since 2019. Considering that appraised values are like market prices, this suggests that recently, prices in the auction market are lower than in the sales market.

Savvy investors are turning their attention to the real estate auction market to exploit niche opportunities. If they can properly analyze the real estate market and identify undervalued areas, they will be able to fully enjoy excess returns in the auction market.

Bubbles can also occur in the auction market

A question naturally arises: Can bubbles occur in the auction market just like in the sales market? To answer this, we need to understand the real estate auction market in Korea.

In Korea, auctions are widely perceived as a way to buy real estate at a lower price. However, one peculiar aspect of the Korean auction market is the frequent occurrence of the so-called “Winner’s Curse,” where the winning bidder ends up overpaying due to overestimation of the property’s value or intense competition. This phenomenon is often attributed to Korea’s unique real estate auction system, which sets it apart from those in other developed countries.

Korea’s real estate auction system employs a sealed-bid auction and a first-price auction format. In a sealed-bid auction, bidders cannot see the prices offered by others, ensuring independence between participants. In the first-price auction, the highest bidder wins and pays the amount they submitted. Bidders aim to submit a price lower than the market value but higher than their competitors, so the bid prices generally don’t vary greatly. Unless the bidder is a stakeholder, such as a tenant or creditor, it is rare for someone to submit an overwhelmingly higher bid than others.

However, if current real estate prices do not accurately reflect intrinsic value, or if expectations of future price increases take hold in the market, the situation changes. Market participants, anticipating excess returns, will flood into the auction market, leading to intense competition. As a result, the gap between the winning bid and the second-highest bid will widen significantly. Moreover, as bidders are driven by herd effect and inflate bid prices, this phenomenon closely mirrors the bubble seen in the real estate sales market.

In addition, the real estate auction market is known to precede the sales market. As we observed earlier, when real estate prices begin to rise, properties listed in the sales market often move to the auction market at lower prices, activating the auction market. Therefore, if we can detect a bubble in the auction market through data analysis, it could also serve as an indicator to identify a bubble in the real estate sales market.

Ⅳ. Bubble index: Price Differences between the 1st and 2nd Place Bids in Auction Market

Literature review

Previous studies on predicting real estate market prices or auction winning bids have employed the Hedonic Price Model and Time Series Model. The Hedonic Model is a regression model based on the assumption that the price of a good is the sum of the quantities of its inherent characteristics. In prior research, the focus was on increasing accuracy by adding as many variables as possible that could represent the characteristics of real estate. However, adding a large number of variables poses a risk. Including unnecessary variables without sufficient validity can lead to multicollinearity, which increases the variance of the estimates and results in unreliable outcomes. This is also the reason why research using the Hedonic Price Model has not been conducted since the mid-2010s.

Data and variable selection

In this study, we aim to address the issues found in previous research by introducing the price differences between the 1st and 2nd place bids in the auction market as an indicator of a bubble and statistically verifying this index.

In this study, the data consists of the quarterly transaction volumes from 2014 to 2022 for the Gangnam and Nowon districts. These areas were deemed most suitable for the study, as Gangnam and Nowon are the regions in Korea with the most active transaction and bidding activities.

Additionally, while this study is based on the Hedonic Price Model as a foundation, it introduces some modifications. The dependent variable is the corrected winning bid rate(y), while the independent variables include the number of unsuccessful bids(FB_NUM), the number of bidders(BD_Num), the bubble index (Index_5), and the M2 currency volume(M2), distinguishing the variable selection from previous studies.

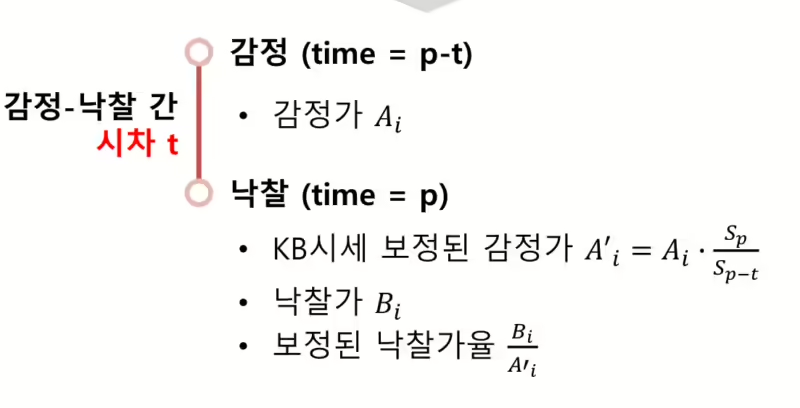

To elaborate on the dependent variable, the corrected winning bid rate, the original winning bid rate is calculated by using the court appraised value (typically the KB market price) as the denominator and the winning bid as the numerator. However, there is a time gap of about 7 to 11 months between the appraisal and the winning bid. Therefore, this study adjusts the court appraised value, which is the denominator in the traditional winning bid rate, to reflect the market price at the time of the winning bid using the following formula.

To further explain the independent variables in this regression model, first, the number of unsuccessful bids(FB_NUM) serves as a control variable that explains auction risk factors. A high number of unsuccessful bids indicates that the auction price is set higher than the market price, leading participants to forgo the auction. Consequently, this suggests a higher likelihood that the next auction will also fail. Second, the number of bidders(BD_Num) refers to the number of people who participated in the auction. As market overheating(a bubble) occurs in the auction market, the number of bidders tends to increase, making it a potential indicator of a bubble. Third, the price differences between the 1st and 2nd place have been explained several times before, so it will be omitted here. Lastly, the inclusion of the M2 currency volume(M2) in the model considers the general trend that an increase in money supply often leads to a sharp rise in real estate prices.

Exclusion of the Intrinsic Value of Real Estate and the Necessity of the Chow Test

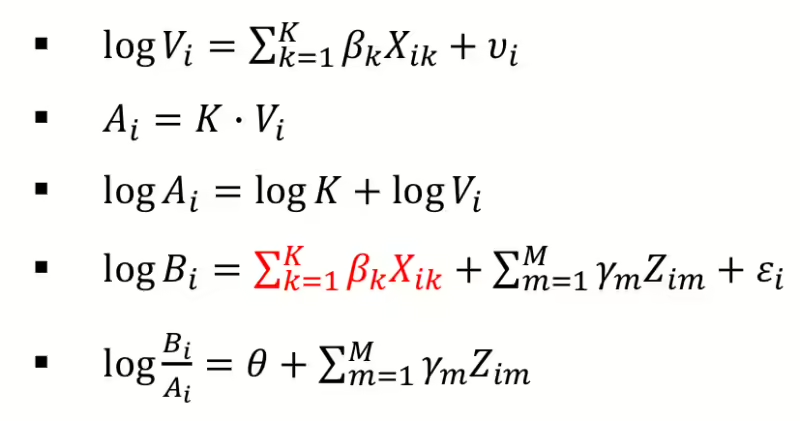

There are numerous factors that determine real estate prices, such as school districts, job opportunities, apartment floor levels, proximity to roads, building age, apartment structure, and transportation convenience. These elements that influence intrinsic value are extensive and complex. Therefore, in the regression model for the corrected winning bid rate, I applied a logarithmic transformation to eliminate the intrinsic value, allowing the focus to remain solely on the auction characteristics, which is the main purpose of this study. The detailed process is as follows.

This paper also assumes that a structural break occurs when a bubble forms, so conducts a Chow test to verify this. The assumption is that during periods of market overheating, such as a bubble, the market will behave differently due to irrational investment sentiment compared to other periods. The Chow test is a statistical test used to determine whether there has been a “structural shock or change” by comparing the regression coefficients of two linear regression models before and after a specific period in time series data.

Regression Analysis and Chow Test

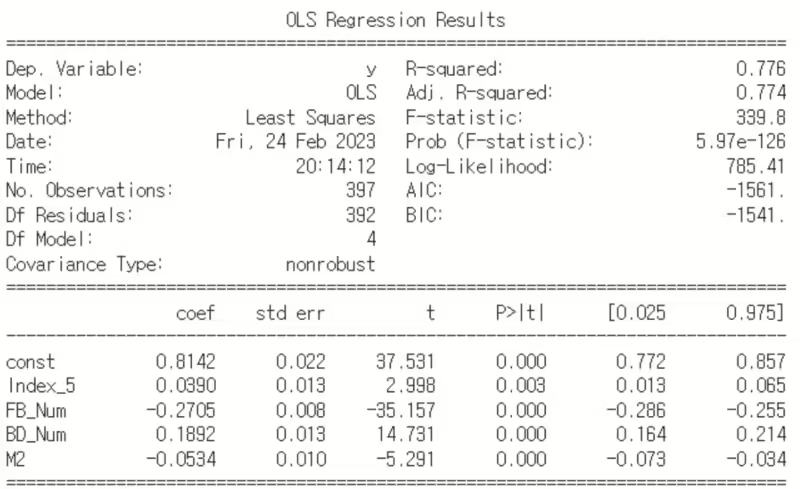

First of all, I conducted regression analysis over the entire period. The dependent variable is the corrected winning bid rate(y), and the independent variables are the number of unsuccessful bids (FB_NUM), the number of bidders (BD_Num), the price difference between the first and second bidders (Index_5), and the M2 currency volume(M2).

As shown in Figure 5, the adjusted R-squared is 0.774, and all independent variables are statistically significant. One notable point is that in the regression model for the entire period, the coefficient for Index_5 (the price difference between the first and second bidders) is 0.039, indicating that it has a relatively small impact on the winning bid rate compared to the other independent variables.

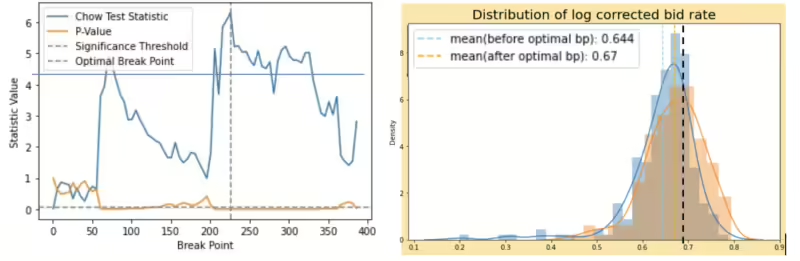

Next, let’s identify the structural break point through the Chow test. As shown in Figure 6, it can be statistically confirmed that a structural break occurred at point 226 (Q2 2016).

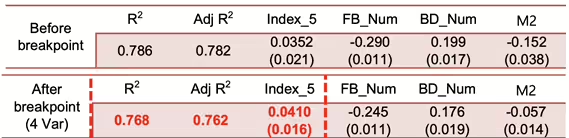

Let’s divide the data into two regression models based on the structural break at point 226 and examine whether there is a significant change in Index_5(bubble index) before and after the structural break.

As seen in Figure 8, Index_5 was not rejected at the 0.05 significance level before the structural break, but after the structural break, Index_5 (t-stat = 2.613, p-value = 0.01) became statistically significant. This indicates that the bubble index (Index_5) significantly increased at the point where the actual bubble occurred (the structural break point).

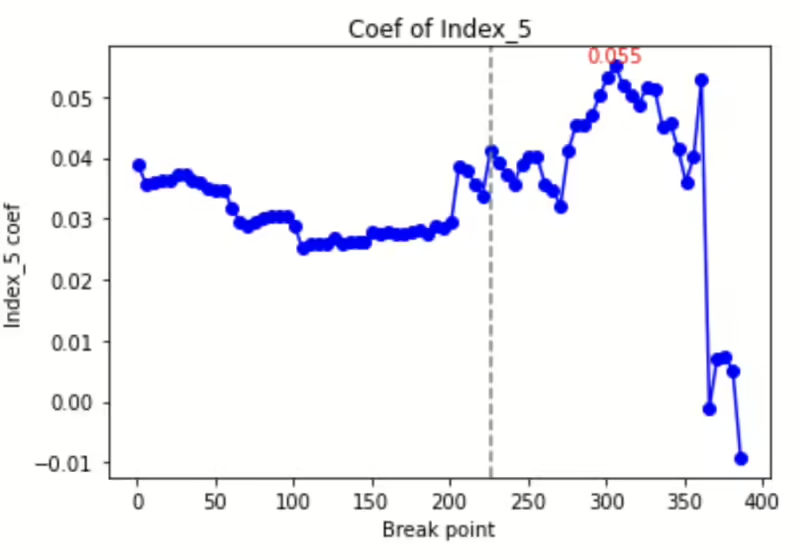

Figure 9 also shows that Index_5 began to fluctuate significantly around the structural break point at 226. After point 226, there was a notable increase in Index_5, reflecting the overheated real estate market at that time, as liquidity in the low-interest-rate environment flooded into the Gangnam reconstruction market and new apartment developments in Q2 2016.

For this reason, I argue that the price difference between the first and second bidders can be used as a bubble indicator. By utilizing this metric, we can prevent the bubble from inflating further and take action before the bubble bursts unexpectedly, leading the real estate market into a downturn.